Nimbility’s Ian Ford’s analysis on what is really going to happen in China

Link to original article

It’s understandable if your focus and interest in China has waned a little over the last few months as its on-going issues with Covid and travel has meant the imported wine market has taken a hammering. But China is not a market we can ignore for long and even if sales have slowed down considerably the potential and opportunity is still there. To get a true insider’s view of what is really happening we turn to Ian Ford, founding partner of Nimbility, and widely recognised as one of the most authoritative and important independent commentators and analysts on the Chinese wine market.

Based in Shanghai, Ian Ford is ideally placed to give a first hand account of what is really happening in China, and the wider Asian markets, as part of the business analysis and brand development services that Nimbility offers.

You can watch Ian Ford’s full analysis on the Chinese wine market here.

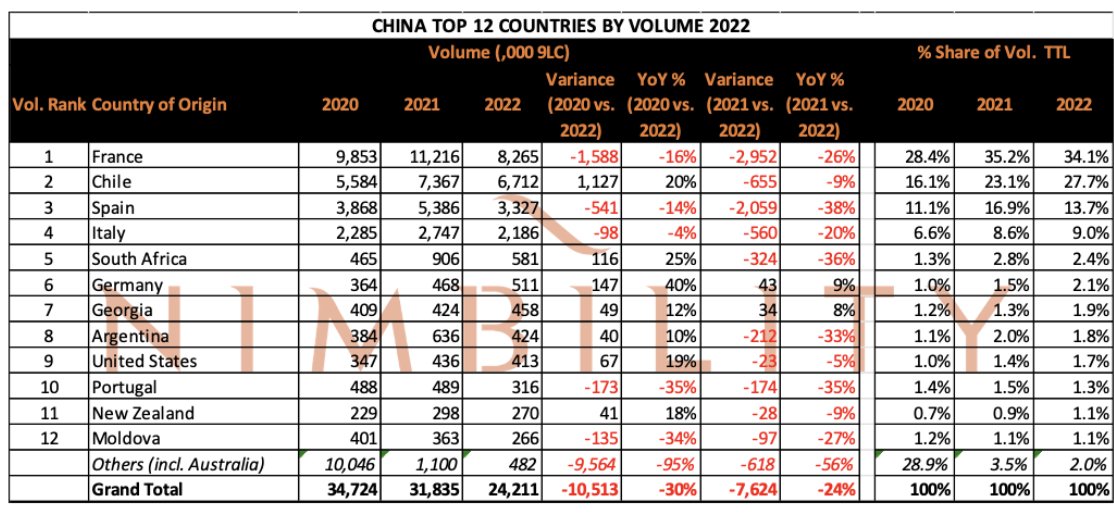

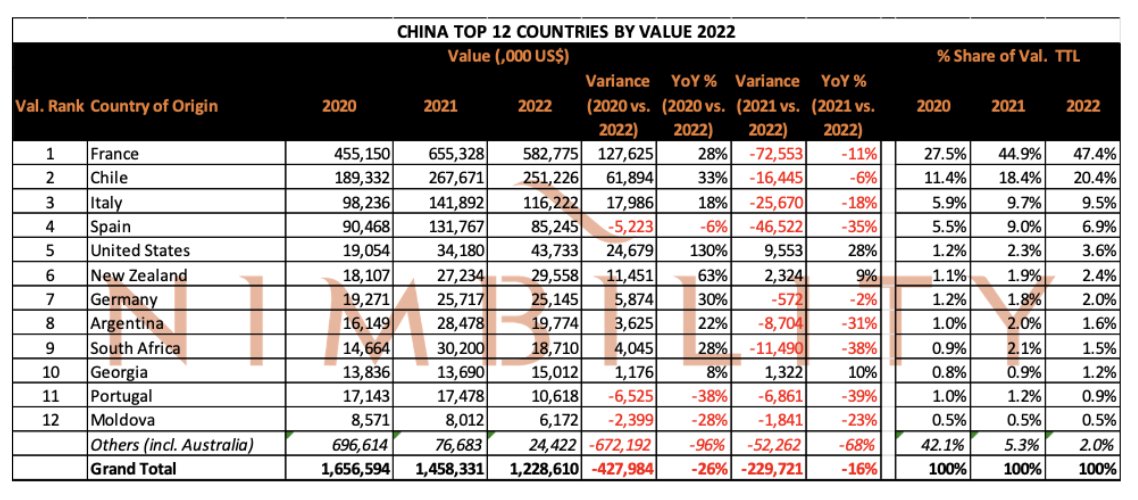

2022 was the most challenging year for imported wines in China in any time over the last 30 years. With rolling lockdowns and testing requirements across the country for the entire year and a two-month complete shutdown of Shanghai in April-May 2022, which effectively crippled all of China’s wine logistics, the challenges were multiple, country wide and unprecedented.

Not only were supply chains, logistics and warehousing severely disrupted but the market closed in terms of demand. In Shanghai, for example, everything was shut for more than two months from March 2022 – bars, restaurants, hotels, grocery stores, convenience stores and then the lockdowns were rolled out across the rest of the country until November. Major events, conferences, exhibitions and meetings were all being continuously planned and postponed and planned and postponed. Consumers became very conservative with their spending.

This is reflected in the year’s topline import statistics for still bottled wine by volume and value:

2023 expectations

Q1 is expected to be volatile for imported wines in China but the near to medium term looks more positive for the market in general despite the continuing hefty tariffs on Australian wine. Nimbility predicts a rebound from Q2 and into Q3 now that China has scrapped its Covid zero policy although the impact of 2022 will still be felt in the first quarter of 2023.

The consensus is that the first quarter will be a recovery period. The importers are all quite wounded from last year and they’re going to be dealing with cash flow pressures and very volatile inventory positions and trying to get the wine trade infrastructure wheels back in motion. It’s not like you flick a switch on zero Covid and suddenly all the importers are fine. People are also still concerned about the spread of Covi which has a dampening effect on consumer behaviour. But I’m cautiously optimistic.

With the zero Covid policy now scrapped in China and in-bound travel for business slowly returning, we are seeing an increase in meetings, trade fairs and conferences as well as things like big sporting events which will all contribute to increased economic activity within the country and set China on course for a significant rebound, presenting plenty of opportunities for wine producers.

Chance to shine

China will once again offer a huge opportunity for imported wine once the dust settles on Covid lockdowns, says Ian Ford

Concurrently, a shift in the market landscape off the back of three years of Covid and the punitive tariffs placed on Australian wine is opening the way for a multitude of new listings and opportunities in the market. Now is a good time for wine producers to lean into the market and actively seek out those opportunities.

For brands already in China it’s time to look to reignite the market and for wineries to take a fresh look at what China can offer. It’s the ideal time to do a brand health assessment to review where a brand currently sits in the market, taking a look at elements such as current pricing, route-to-market, brand building activation and visibility, digital presence, competitor benchmarking and IP & Trademark registration.

Now is also the time to be engage actively with importers, talk to them about the year ahead, their plans, and explore potential opportunities in the market and how you can offer support. At the root of the matter is demand creation, building brand and creating genuine consumer demand.

It’s also a good time to look at the digital space in China and look at how brands live in this space and on platforms which are very unique to China such as WeChat, Douyin and RED.

Australian woes

Treasury’s growth in Asia, driven by its Penfolds brand, can quickly return once the imported market comes back, says Ford

There is a lot of talk of tariffs on Australian wine being lifted but I don’t see any hard evidence of these being removed. That said the longer-term prospects for Australian wine imports into China remain strong. Anything is still possible if there are really genuine attempts to warm up relations between Australia and China. If the tariffs are rescinded the taboo around Australian wine would turn around quite quickly and there wouldn’t be any long, lingering effects.

Treasury Wine had established a real powerhouse business in China before the introduction of the tariffs and if the tariffs are reversed it will become a very substantial market for it again. It’s maintained a core team here in China – some really good talent – that’s focused on managing the South African and California products but obviously not Australian wine at the moment.

Other markets around Asia are growing, especially South Korea where Nimbility has just established an office, but their markets will always be dwarfed by China. The last time the Chinese market was in a normal state it was around 50-60 million 9 litre cases of imported wine and I think the market could be twice that in 10 years.

It’s still relatively early days for imported wine in China. I think if you look at per capita consumption, the trade infrastructure, the actual real true availability of imported wine, the penetration across the market, China’s very dynamic beverage alcohol sector and the fact that the Chinese dining occasion is absolutely suited to imported wine…if you look purely at the size of the population, there’s still a long way to before China will be a saturated market for imported wine.

The opportunity is still massive but as always with China, it’s never simple and never easy.

For more detailed information on the China market or Nimbility’s Brand Health Assessment China service, please contact chess@nimbilityasia.com.